Taiwan’s Solar PV Market Continued to Grow in 2018 and Surpassed 1GW in Installations for the First Time

According to the newest Regional Project Report –“Solar Powering Taiwan: Special Report” by EnergyTrend, a division of TrendForce, 2018 will prove to be the most disastrous year for Taiwan’s solar PV manufacturers, yet the best year in terms of solar PV system installations downstream, bringing new installations up to 1GW for the first time in history. The government is now actively pushing towards a goal of 1.5GW in new installations by the end of 2019.

Judging from the rankings of and the positions taken up by module, inverter, downstream EPC contractors and bank and life insurance companies in 2018, EnergyTrend analyst Sharon Chen points out that though the market scale for PV systems aren’t as large as that of wind power, the PV market has already undergone a long formation process. Consider further the fact that PV charging stations have a relatively steady and high return on investment, and it’s not hard to see why even banks and life insurance firms are scrambling to claim a portion of this market.

URE Modules Take Up Nearly Half the Market, While AUO Stands Firmest due to its Global Strategy

The module market of 2018 differed from 2017’s, which saw Neo Solar Power (NSP) and AU Optronics (AUO) as the leading double eagle. URE benefited greatly from its three-in-one strategy, with NSP as the surviving company combining both Gintech and Solartech to become the top contender by module shipments in Taiwan, 2018: It reached 500MW in total shipments, with market shares leaping from 30% in 2017 to 48% in 2018.

In comparison to URE, AUO maintained a global, overseas strategy, ensuring a consistent number of yearly shipments. This put its 2018 shipments on a par with those in 2017, fully demonstrating its global strategy as the most stable among Taiwan module manufacturers.

It is worth noting that Canadian Solar Inc., which stepped onto Taiwan soil in 2018, catapulted to sixth place in shipments under a half-year, and is predicted to claim up to 20% share of the Taiwanese market in 2019.

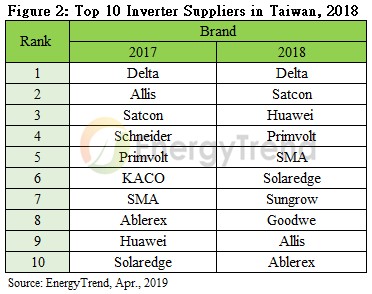

Delta Electronics Exceed 1GW in Inverter Shipments in Taiwan, with SMA Market Shares Maintaining Steady Performance

The annual number of new installations of PV systems in Taiwan reached 1GW for the first time in 2018, nearly a one-fold increase from 2017 (520MW). Thus shipments for all vendors doubled in the inverter market. But competitors are rushing in as the market expands, splitting the market shares of pre-existent products. Apart from SMA, whose market share in the Taiwan region remained sure and steady, inverter manufacturers at home and abroad all experienced a decline in market shares in 2018, including Delta.

Delta still holds first place in inverter shipments for 2018. Although its market shares dropped by 10% compared to 2017, it nevertheless boasted double the shipments of second-place company, Satcon, which has Skwentex acting as sales representative in Taiwan, and reached this position in shipments thanks to the 100MW demonstration program carried out by the Renewable Energy Department under Taiwan Power Co.